NFTs can now serve as court documents… but they might also be unregistered securities, illegal loot boxes, or come with impossible tax demands.

Nonfungible tokens (NFTs) are thought of by most people as just funny pictures that degens on the internet spend far too much money on for poorly understood reasons. But Jason Corbett, managing partner of global blockchain law firm Silk Legal, says new and innovative use cases are beginning to emerge.

“We’ve seen recently the courts allowing the serving of court documents by way of an NFT,” Corbett says, referring to a recent decision by a United Kingdom court to allow notice of the case to be served by airdropping court documents as NFTs to wallets allegedly stolen from the claimant.

This changes our conception of what NFTs are and what rights and responsibilities come with them. Following this precedent, the sending of NFTs can be understood as a type of electronic communication, with the caveat that it is generally public. The sending of NFTs is more comparable to attaching posters to the outer wall of one’s house versus discreetly sliding them into the mailbox.

This comparison to publicly visible posters begs the question of whether this means that individuals controlling blockchain wallets hold responsibility for the NFTs they hold, in the same way as a homeowner would ultimately be responsible for removing obscene or otherwise illegal posters on their property, even if placed there against their will.

Does this mean that, for example, the owners of wallets may in the future be responsible for monitoring them for any type of illegal content sent to them, and act quickly to dispose of them in some manner? That’s just scratching the surface.

Metaverse Law MA thesis “ENCODED TERRITORY: The Blockchain-based Metaverse as a Special Environment of International Law” argues that the #Metaverse influences the balance of global power & demands special legal treatment @UniTurkuLaw @UniTurku#NFTs #BlockchainGaming #cryptolaw pic.twitter.com/GSvghv6Xoy

— Elias Ahonen.eth (@eahonen) June 11, 2022

“The blockchain Metaverse presents challenges to the international order due to the limited ability of states generally to intervene in metaverse-based actions,” I wrote in my Master’s in International & Comparative Law thesis, “The Blockchain-based Metaverse as a Special Environment of International Law.” One fascinating, and perhaps off-putting, matter that has continued to come up in my research is the lack of clarity and, at times, the absurdity of earthly legal matters when applied in, and to, the metaverse.

NFTs and cryptocurrencies are a good place to begin exploring the subject, seeing they are effectively the building blocks and lifeblood of the metaverse. Both are, of course, tokens — one being nonfungible in the sense that they are unique “items,” with the other being fungible “energy” with which the metaverse operates. By metaverse, we of course refer to the blockchain-based version of it, not some corporate-controlled Fortnite version.

Securities regulations

A variety of cryptocurrencies, often known as tokens or coins, began to appear in 2011 as theoretical alternatives to Bitcoin. Growing in prominence, they had their day in the spotlight during the initial coin offering (ICO) boom of 2017, during which hundreds of projects attempted to raise money by issuing tokens to investors.

When hundreds of millions of dollars are being raised in an entirely new way, it’s not surprising that potential legal concerns are lurking around the corner. This was certainly the case with ICOs, which regularly ran afoul of securities laws and the related accredited investor laws, says Randall Johnson, a United States lawyer with 30 years of experience specializing in securities regulations and who advises various blockchain projects.

What will be the law of the metaverse? . The legal and ethical dilemmas plaguing technology today will only grow more acute in the metaverse, writes Brian Harley. How will real-world laws apply?

— Nathan (@shanzi73338680) August 28, 2022

He explains that one of the key questions around whether a token can be classified as a security is whether “the general public would think it is an investment.” This means that white papers or presentations that boast that tokens are “already on exchanges” or, worse, openly describe them as “good investments” and use “to the moon” style boosterism, are painting targets on their backs. Another factor that almost always makes a token a security is “if it operates like a dividend-paying share in a company,” he explains.

“A large part of regulator analysis on whether a token might be a security has to do with how it is advertised and promoted.”

But how is the financial regulation of cryptocurrencies related to the metaverse and NFTs? It’s because NFTs are tokens just the same, and serious questions could arise regarding their status as securities.

What some may view as art might look like little more than stock certificates emblazoned with digitally generated monkey pictures to regulators. Indeed, Johnson himself is co-founder of LiquidEarth, a platform that is turning title deeds into income-producing real estate from around the world into NFTs.

His companies do not fractionalize the deeds because “then the NFT is by definition a security,” he asserts. The long-term goal is to create a “global real estate exchange” where one could seamlessly invest across borders, with the actual deeds held in trust.

James Woolley, chief marketing officer of Metavest Capital, agrees that while most NFTs do not resemble securities, others are likely to get caught in regulator’s nets.

“There are variations of NFTs that will struggle to pass the Howey Test — fractionalized NFTs where there is a ‘lead role’ played by a marketplace or exchange will likely be more formally regulated by the Securities and Exchange Commission.”

Woolley also mentions worrying speculation that the SEC under Gary Gensler, which has remained tight-lipped on the issue beyond declaring Bitcoin a commodity, has its aims on declaring “all other fungible and nonfungible tokens” as securities — a move that would do untold damage to the industry.

Other experts worry that Web3 innovation has left appropriate regulations far behind.

“Regulatory authorities worldwide are failing to keep up with the rapid technology developments in the Web3 and the metaverse space,” concludes Irina Heaver, partner of Keystone Law specializing in blockchain industry and general partner of VC investment firm Ikigai Ventures.

In her work, Heaver describes regularly hearing concerns from regulators because innovative new crypto business models “inadvertently trigger existing regulations concerning banking, lending, capital formation and other activities which were traditionally the domain of large players, such as banks.”

“Developers can code faster than any regulator can regulate.”

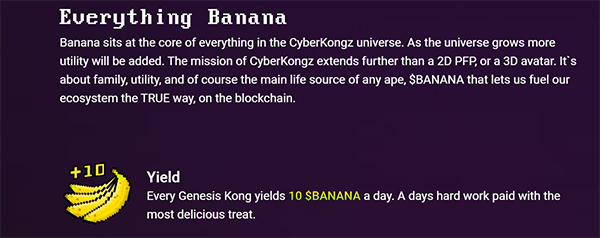

Yes! We have no bananas

One example of possible triggering of securities regulations may be found in yield-bearing NFTs. Take for example CyberKongz, sometimes credited as the first NFT monkey collection, whose 999 “Genesis Kongz” “yields 10 $BANANA a day,” according to the site, in reference to the project’s cryptocurrency.

At the project’s height, this meant that each monkey-holder earned the equivalent of over $700 per week. In this case, would it not be unreasonable for a regulator to consider each CyberKongz NFT the equivalent of a class-A share paying daily dividends on the project? It’s still a gray area, but the possibility is not entirely closed off.

If such a precedent is established, it could open a Pandora’s Box regarding what the extent of securities regulations could be.

Suppose an artist creates an NFT series titled “An Artist’s Share” whose 100 unique works are then included in smart contracts designed to automatically pay the owner of each “Artist’s Share” a 0.1% payout of the given artist’s gross revenue from minting and royalties. Would this be a mere NFT, or would it be a security? According to Johnson’s definition, it would seem to fit the bill. Could simple airdrops of new art to existing collectors also fit the bill?

Taxation quagmire

Even where NFTs may not be securities, there are serious uncertainties regarding how and on what basis they can be taxed.

Consider a hypothetical blockchain game, where a player can begin playing for a small cost of $20. With time, however, the theoretical value of their in-game items (NFTs) may grow. Does the mere playing of a metaverse game thus entail potentially hundreds of taxable events per day, leaving an unsuspecting player on the hook for preparing tax returns comparable to those of a medium business in complexity?

An example of this can easily be found with Axie Infinity, which, at least until recently, had a massive player base in the Philippines. Mark Gorriceta, managing partner at Filipino law firm Gorriceta Africa Cauton & Saavedra, said that in the country, NFTs have become “mainstream due to the rise of play-to-earn games like Axie Infinity.”

Cointelegraph previously reported on the country’s Finance Undersecretary Antonette Tionko commenting regarding the play-to-earn model that “whoever earns currency from it, it’s income you should report it.” However, this seemed to only refer to the act of actually selling in-game assets (NFTs) or in-game “points” (SLP and AXS tokens) for fiat currency or other tokens.

What is left unclear is what happens if a player, for example, finds a rare in-game item whose external market value is $100,000. If they simply elect to use this item in a game, will simply having the rare item come into possession be seen as a capital gain?

If not, would the situation change if they trade, exchange or somehow convert the item into something else within the game — such as using a “magic metaverse log” valued at $100,000 to manufacture in-game planks with which to build an in-game house to boost the character’s in-game building score? Just how many taxable events could an in-game activity like this entail?

Consider a real-world example of finding a gold bar while walking on a beach — in some tax systems, you might be forced to pay tax on it that year, potentially meaning that the bar needs to be sold in order to raise the money necessary to pay taxes. Even in jurisdictions where no taxes are owed because simply keeping the gold bar results in no realized gains, things generally change as soon as the bar is bartered for a new car or luxury watch, even if no fiat money was involved. Even personally smelting the bar into personal-use jewelry could spark a taxable event.

This, of course, opens a new can of worms entirely — tax authorities would need a system by which to actively evaluate the market value of various, often unique NFTs. Perhaps NFT appraisers will be one of the new metaverse jobs accounting firms around the world will soon be hiring for.

Wealth taxes for NFT collectors?

Speaking of the market value of NFTs, questions arise regarding various forms of wealth tax that are present in various European countries, such as Norway, where residents must annually pay 0.85% of the value of their net worth exceeding $170,000.

This means that each year, Norwegians should estimate the total value of their NFTs, whether game items, art, metaverse real estate, ENS domain names, or good old monkey pictures. While a floor-level Bored Ape Yacht Club NFT worth $100,000 would incur $850 in annual taxes, how much does the owner of a monkey with rare features like laser eyes or gold skin need to dish out? What about subjectively desirable numbers such as Monkey #8888 or #69420? No one knows, but the Norwegian tax office will expect their due regardless.

Continuing with the Axie Infinity example, the metaverse’s mode of operation introduces certain territorial absurdities when it comes to taxation. For example, the Philippines has territorial taxation, which means that, for example, an Australian citizen living in the country would need to pay taxes only on income they earn from the Philippines, while income from elsewhere remains effectively tax-free.

This means that the hypothetical Australian playing Axie Infinity in the Philippines would need to know the tax residency of every person they are selling their NFTs to, especially considering such a large portion of the player base is indeed within the country.

Determining the tax residency of NFT buyers is, of course, not practically possible in the open and decentralized markets as they exist today. This may become a serious issue in the future, for example, with countries that charge sales tax when goods or services are sold within the country.

Meanwhile, in Australia, there are certain circumstances in which NFT owners may need to pay a 10% Goods and Services Tax, depending on if it’s a Personal Use Asset, a Capital Asset of a business or used as a part of a business.

Though things are still at their early stages, Corbett says that in a few years, tax systems “will be reading what’s happening on blockchain,” referring to advanced versions of tools, such as token.tax, which will be used by both individuals and regulators. The surveillance of exchanges that serve as on- and -off ramps for fiat will also increase, allowing the tax man to uncover positions.

“Tax authorities will start kind of cobbling together what the taxable crypto positions of nationals are.”

Is it possible they will start combing through those immutable records back to today and apply laws and taxes retroactively to current NFT owners? Will there be a new generation of prison gangs forming around NFT affiliations — Apes Anonymous, anyone?

In the upcoming FLIP Buzzwords webcast, we explore how the #metaverse impacts legal issues such as personal injuries, copyrights, patents, contracts, claims by users against companies, and claims against other users under crime and tort law. Register: https://t.co/zqBMCOg0nI pic.twitter.com/FHKvoiBOeH

— LawSocietyNSW (@LawSocietyNSW) August 24, 2022

Loot boxes and gambling

Many countries regulate gambling, which would likely include metaverse-based casinos. Some governments even place restrictions on the inclusion of purchasable loot boxes in video games, often citing a desire to prevent young people from gambling.

This is likely to become a concern with play-to-earn games, where loot boxes might take the form of NFT minting.

This raises wider questions over whether NFT minting itself could be considered a legal equivalent to loot boxes or gambling in general. This is because NFT minters often pay significant sums of money in hopes of getting a particularly rare or valuable version of the NFT being minted.

Beyond loot boxes, one might be concerned whether the entire play-to-earn model, where players can be understood to bet money in various ways, might itself be classified as gambling with a broad brush. Woolley, however, is optimistic, explaining that in 2012, a U.S. federal judge ruled “ruled that poker is not gambling under federal law because it is primarily a game of skill, not chance,” a model he hopes will be applied to metaverse gaming.

Despite this, the jury is still out on “whether games like Axie infinity and their successors can be considered gambling — it’s a question that hasn’t been formally answered.” The South Korean government has already banned such games due to gambling fears, but there are signs the ban may be reversed or amended.

Have you encountered strange or bizarre legal questions relating to the metaverse? Feel free to contact the author at eliasahonen@cointelegraph.com to share your story.

Be the first to comment