A loose liquidity environment and new narrative outbreaks are the main determinants of the bull market after the Bitcoin halving.

The high-interest rate environment may last longer than expected but will not end the bull run.Before interest rates significantly decline, non-BTC cryptos’ performance may remain weak for a long time.

Bitcoin Halving: An Old “Meme”?

The Bitcoin halving seems to be one of the oldest “landmark events” in the crypto market. Since 2012, investors have seemed to believe that the occurrence of the Bitcoin halving event would reduce the supply of BTC and drive up its price, leading to the arrival of a bull market in the crypto market.

However, price changes are never solely determined by “supply”. “Supply” affects prices, and so does “demand”. Luxury homes often have incredibly high asking prices; however, if there are no bidders, sellers have to offer discounts to close quickly. During periods when investors are relatively cautious, many luxury homes are even sold at half price or even lower.

The same is true for the financial market. “Scarcity” is always relative; the price of silver once reached $48 in the early 1980s and hit this high again in 2011. However, despite many analysts claiming, “If the supply of silver decreases while the price falls, the silver mine will go bankrupt and bring a series of serious consequences”, the price of silver has not stayed high for a long time.

Silver price movements since 1970. Source: TradingView

Similar views are not uncommon in the crypto market. Many investors believe that after the halving of BTC production, miners’ profits denominated in BTC will significantly decrease. If the price of BTC drops significantly, miners will have to choose to shut down their mining machines, and the decrease in hash rate will make the Bitcoin network no longer secure, which is highly similar to the views of silver investors to some extent.

However, the above views do not seem to be valid.

In 2022, the price of BTC fell by nearly 80% compared to its peak in 2021, but the hash rate did not significantly decrease as a result, instead maintaining an upward trend – which makes the Bitcoin network sufficiently secure. Even though the hash rate is far higher than that of 2017, there have been no significant security incidents on the Bitcoin network.

Changes in Bitcoin hash rate since 2017. Source: The Block

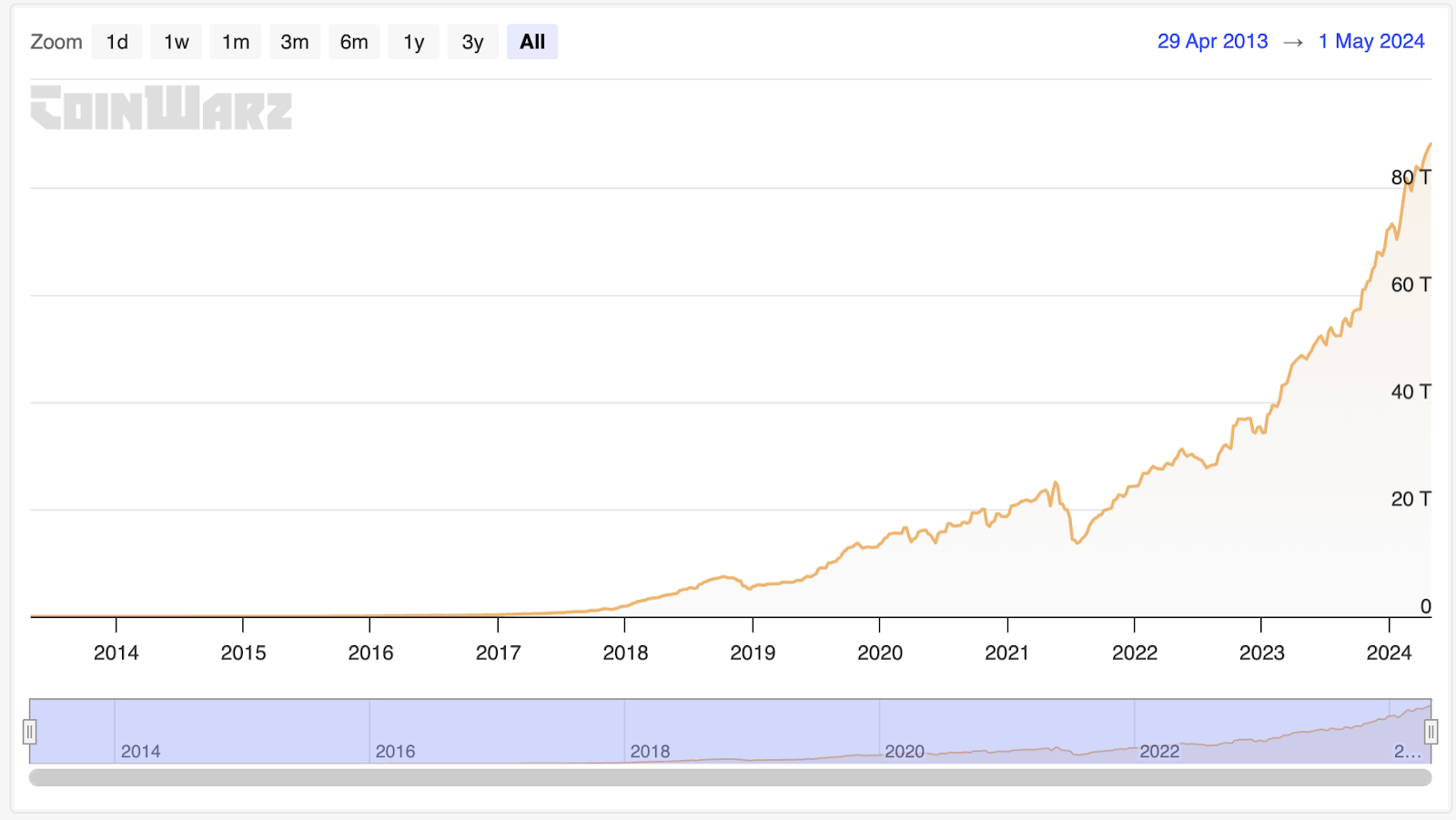

In addition, the mining difficulty of BTC has also changed with the market environment. When the market environment is deeply bear, the mining difficulty will decrease, allowing surviving miners to maintain operations. However, BTC is not infinitely supplied and will be mined out at some point in the future. At this time, how will miners maintain the Bitcoin network?

Changes in Bitcoin mining difficulty since 2014. Source: CoinWarz

Transaction fees seem to be one of the answers. If we only consider maintaining the security of the Bitcoin network, the “astronomical” hash rate is not a necessary condition. Perhaps many miners will quit due to “poor returns, ” but the hash rate and transaction fee income eventually reach a balance.

Considering that the active level of the Bitcoin network has been maintained at a relatively stable level since 2018, and the store of value property of BTC further enhances this stability, in the future, miners who “rely solely on fees” may become the leading force in maintaining the Bitcoin network.

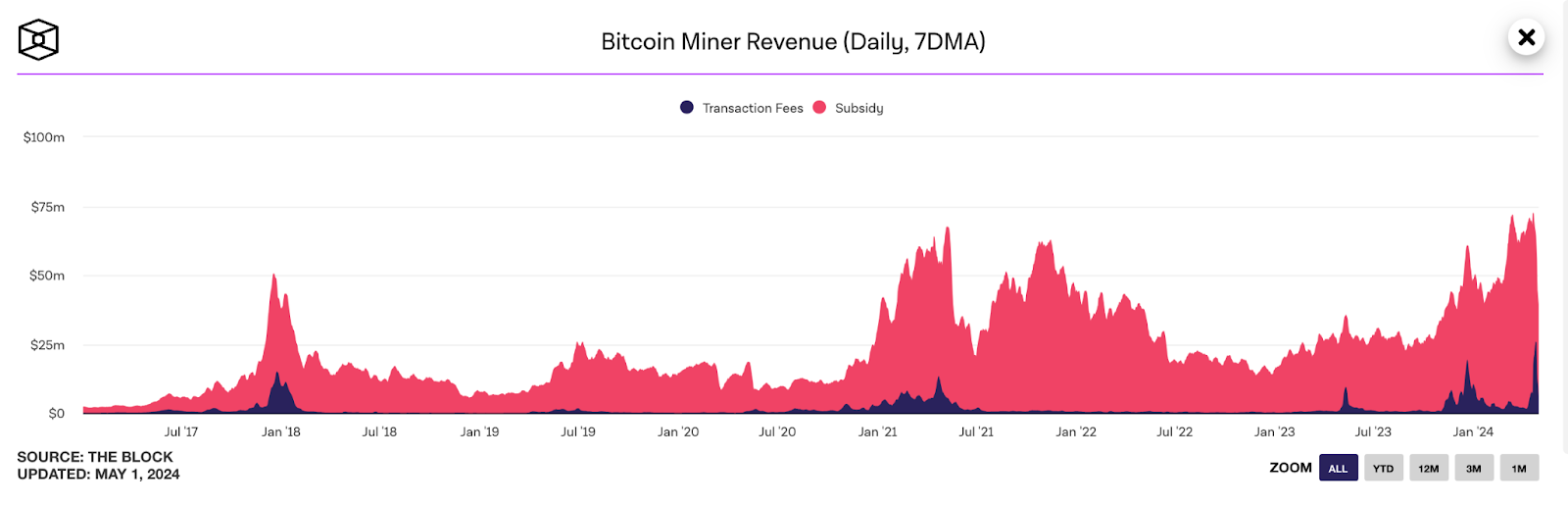

In fact, in April 2024, there were moments when BTC miners’ fee income briefly surpassed mining income. Therefore, regardless of the BTC price, as long as the user base of the Bitcoin network remains at a certain scale, BTC miners can still earn considerable profits and be incentivized to maintain the network.

Changes in Bitcoin miner revenues since 2017. Source: The Block

Transactions on the Bitcoin network, as of May 1, 2024. Source: The Block

In summary, in the early stages of the development of the Bitcoin network, the halving of BTC may have had a significant impact on the price. Still, at the current stage of development, its influence has been significantly reduced. Even after several halvings in the future, BTC miners will find it difficult to obtain block rewards, and the income from sources such as transaction fees can at least maintain the continuous operation of some BTC miners, thus ensuring the security of the Bitcoin network. Besides, as the USD liquidity obtained by BTC gradually accumulates, attacks on the Bitcoin network also become “economically unfeasible”.

It seems that halving is more like an ancient “crypto meme”. So, what are the core factors affecting the price of BTC? Let’s go back to the macro level and review the background of the macro environment and essential events before and after each halving from 2017 to now.

In 2017, a year after the second halving, the crypto market was in a low-interest rate environment. ICOs (initial coin offerings) also emerged at this time, and the scale of financing in the crypto market expanded rapidly.

In 2021, one year after the third halving, the Federal Reserve maintained interest rates at 0% for a long time due to the need to combat COVID-19. Massive institutions began to invest in the crypto market, and the rise of narratives such as DeFi Summer, NFTs, and GameFi pushed the cryptocurrency market into a “comprehensive bull market”.

In summary, the loose liquidity environment and new narrative are the two main engines of the crypto bull market, but halving is not.

So, what will happen after the fourth halving this year? Based on the above history, it is not hard to estimate:

In 2025, one year after the fourth halving, the Fed gradually lowered interest rates (albeit slowly). BTC spot ETFs have reached a certain scale, and narratives such as DePin, RWA, and alternative chains may become the engine of a new round of “fully bull market”.

BTC: Long-termism

The macro-environment does not seem optimistic for BTC: the relatively optimistic interest rate cut expectations at the beginning of 2024 have disappeared. With inflation data continuously exceeding expectations, the Fed has chosen to maintain high interest rates and cautiously promote improving the liquidity environment. In the interbank market, traders expect that the rate cut will be kept at about 4 times from 2024 to 2025, with each cut not exceeding 25 bps. The above will undoubtedly slow down the speed of cash liquidity return, and the pace of the bull market may also slow down as a result.

SOFR fixing rate, which directly reflects inter-bank financing costs. Source: CME Group

However, this does not seem to mean the disappearance of the bull market – at least derivatives traders still have positive medium and long-term expectations.

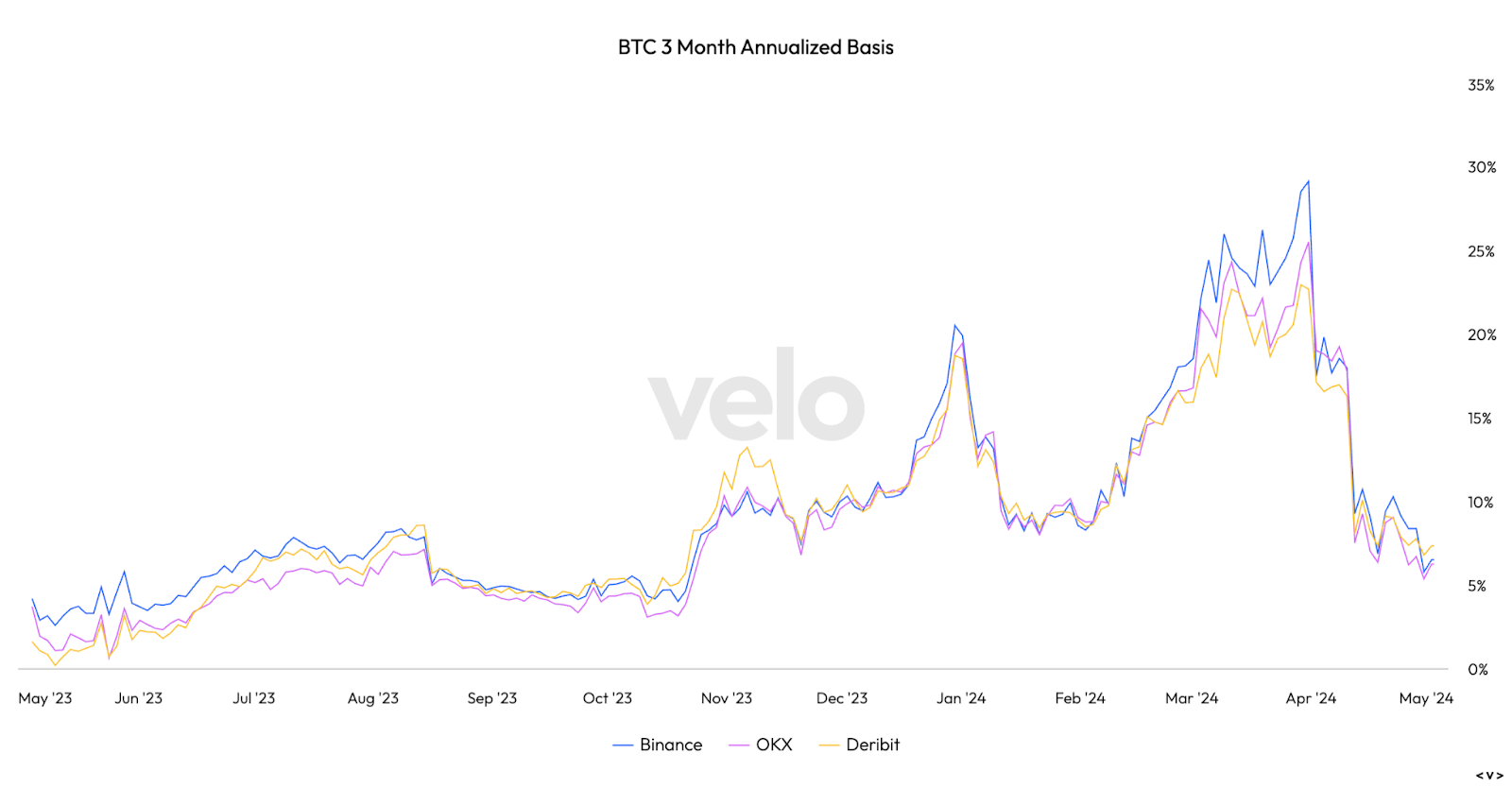

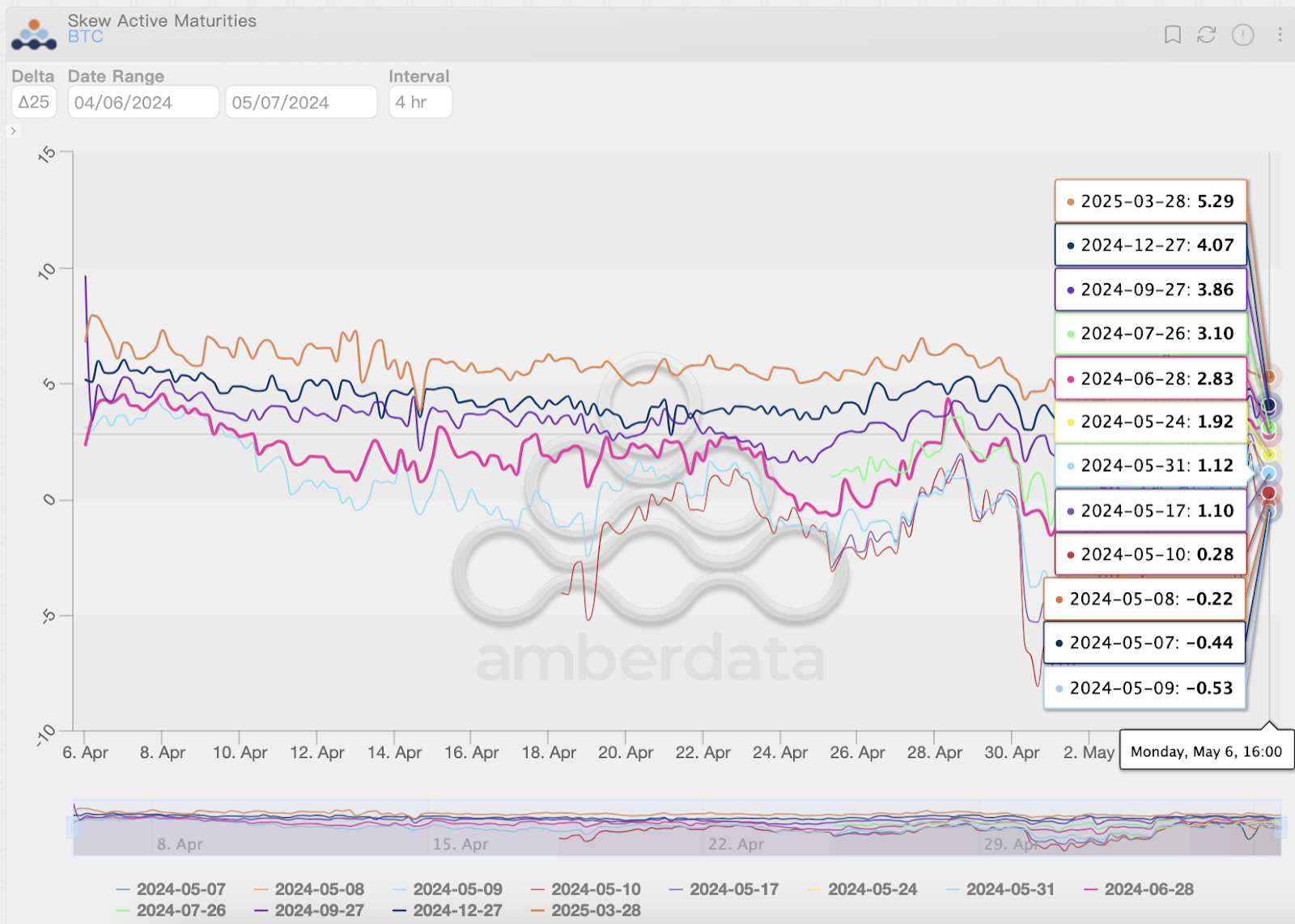

In the futures market, the annualized implied forward rate of BTC futures remains above 7%, which means that investing in BTC is still profitable compared to the risk-free rate, and the risk premium of BTC is still higher than 340 bps. In the options market, although bearish sentiment has gained dominance in front-month options, bullish sentiment in far months has not been significantly affected and has remained relatively stable in recent weeks.

BTC 3 Month Annualized Basis. Source: Velodata

Changes in BTC 25delta skew in the recent 30 days. Source: Amberdata Derivatives

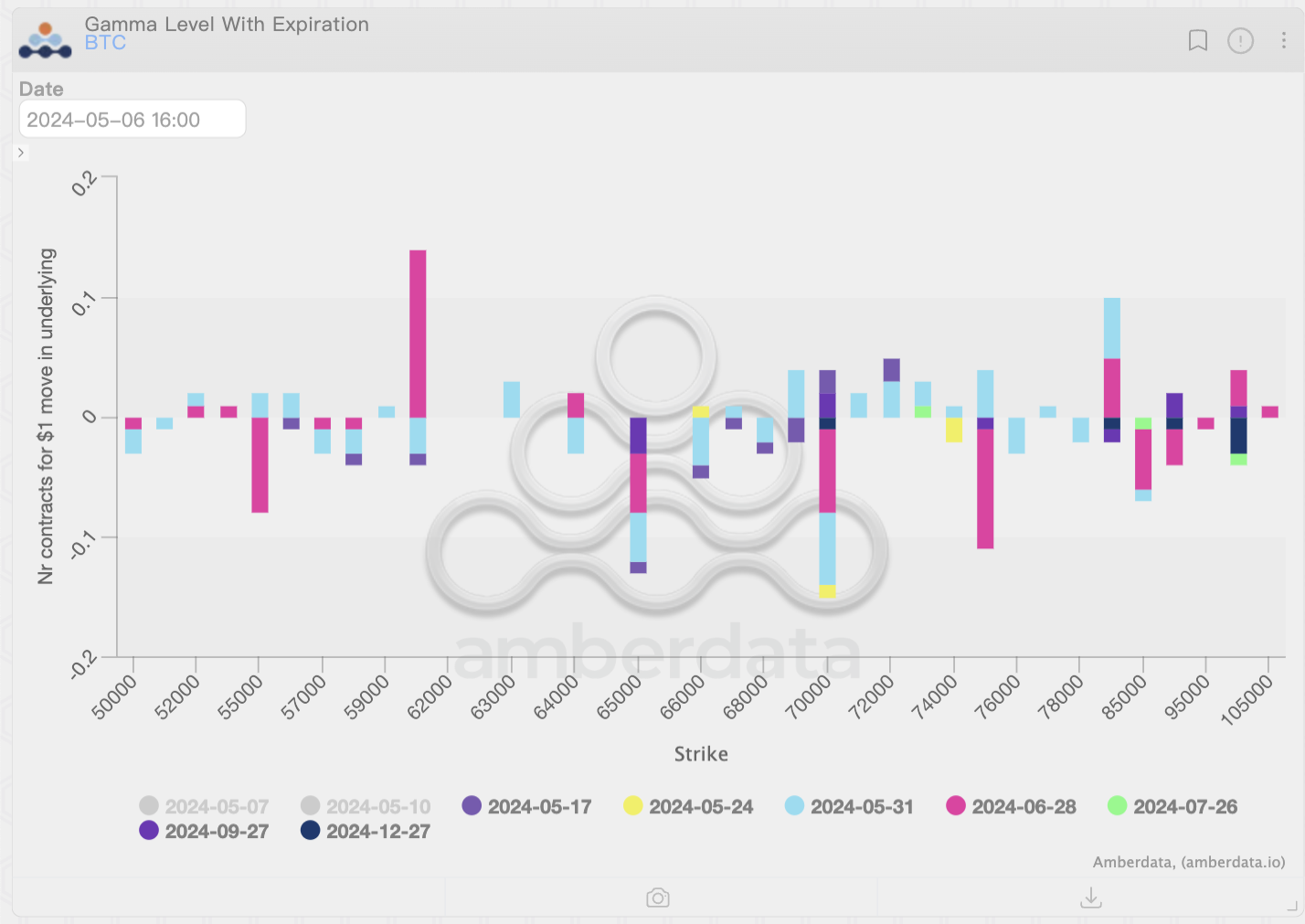

According to the latest gamma distribution, the positive gamma around $60k will have a significant attractive effect on the price of BTC. As the expiration date approaches, the “attractive force” brought by the hedging behaviour of market makers will gradually increase. If the price continues to fall, market makers will also provide some support for the price of BTC.

The latest gamma distribution of BTC. Source: Amberdata Derivatives

In addition, the latest implied volatility data shows that traders expect the 7-day fluctuation range of BTC price not to exceed 7.5%, and the 30-day fluctuation range will not exceed 16%. Therefore, even if the worst-case scenario occurs, the probability of the BTC price falling below $50k is still relatively low, while the likelihood of maintaining around $60k is relatively high. However, there is no doubt that the arrival of a full bull market may be further delayed due to the macro environment. Maybe it’s time to try to be a “long-termist”: hold BTC and wait for interest rate cuts because the macro environment will eventually improve in the next 12-15 months.

ATM boxplots of Bitcoin. Source: Amberdata Derivatives

Non-BTC: Dormant

For non-BTC cryptos, considering their positioning at the end of risky assets, investors’ expectations are becoming more conservative as the bull market slows down. Taking ETH as an example, only options expiring in Dec 2024 and Mar 2025 reflect a certain bullish sentiment, coinciding with the path of interest rate cut. The above situation indicates that investors will invest more in non-BTC cryptos only when the macro environment improves.

Changes in ETH 25delta skew in the recent 30 days. Source: Amberdata Derivatives

The latest gamma distribution also confirms the above view. Due to the lack of upward expectations, investors choose to sell more bullish options, resulting in a steady increase in the scale of positive gamma accumulated by market makers. Without significant positive news (such as the approval of spot ETH ETF), it will be difficult for ETH to surpass the new gamma peak of around $3,300 with the lack of cash liquidity support.

The latest gamma distribution of ETH. Source: Amberdata Derivatives

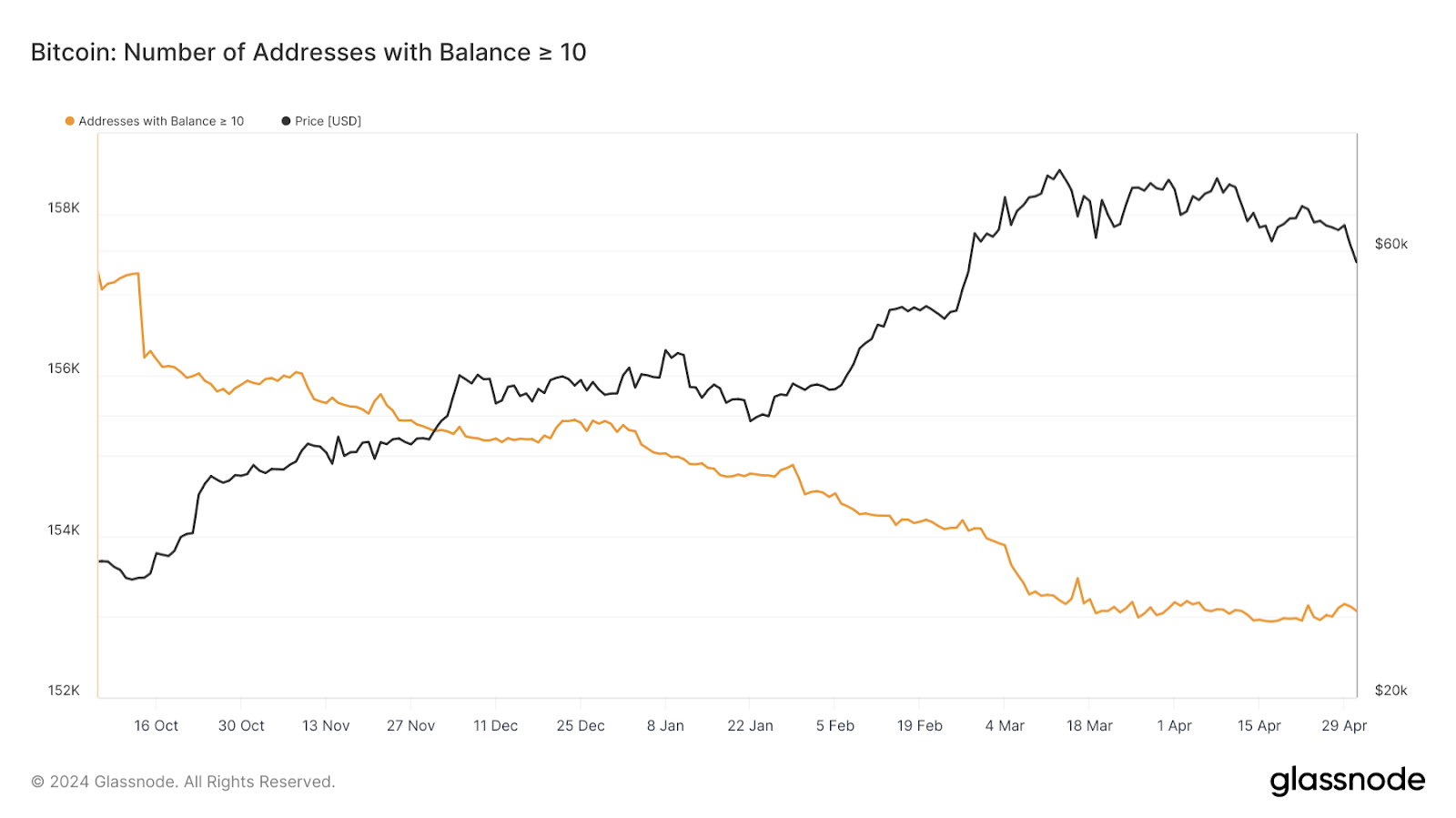

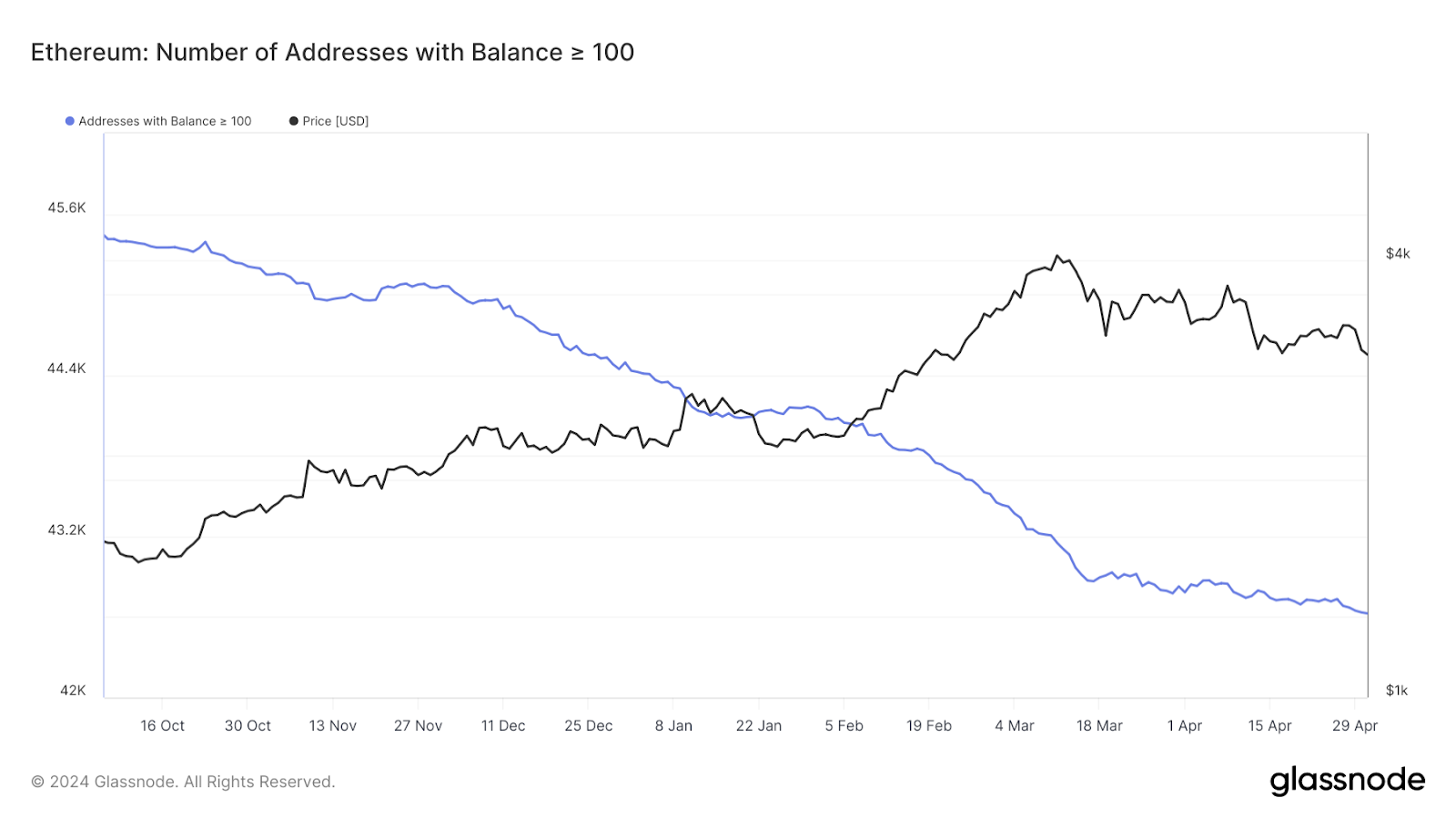

Of course, the whales seem to be reducing their non-BTC holdings. The number of addresses holding more than 100 ETH continued to decline in April; in contrast, the number of addresses holding more than 10 BTC remained stable in April. Even baby whales have realized the changes in the macro environment: they choose to hold BTC and are likely selling ETH.

The number of addresses with BTC balances higher than 10, as of May 1, 2024. Source: Glassnode

The number of addresses with ETH balances higher than 100, as of May 1, 2024. Source: Glassnode

Considering the large number of young whales, the sell-off of non-BTC cryptos seems to have had a widespread impact. The market share of altcoins has fallen to less than 19.5%, while the market share of ETH has remained relatively low in the past year. Since most non-BTC cryptos have difficulty performing well in the “slow bull market” and have relatively higher risks, investment in non-BTC cryptos still needs to be cautious until the macro environment improves. Altcoin warriors, wait for a better chance.

Changes in cryptos’ market shares in the recent 30 days. Source: Coinmarketcap

Disclaimer

This article is sponsored content and does not represent the views or opinions of BeInCrypto. While we adhere to the Trust Project guidelines for unbiased and transparent reporting, this content is created by a third party and is intended for promotional purposes. Readers are advised to verify information independently and consult with a professional before making decisions based on this sponsored content. Please note that our Terms and Conditions, Privacy Policy, and Disclaimers have been updated.

Be the first to comment